In 2022, the Federal Poverty Level (FPL) affordability safe harbor employee contribution amount (for the 48 contiguous states and the District of Columbia) is $103.14/mo or $108.33/month, depending on your plan year.

Applicable Large Employers (ALEs) with 50 or more employees are subject to the Affordable Care Act’s (ACA) provisions that require employers to provide affordable coverage to employees working 30 or more hours per week. If an ALE does not offer affordable coverage, they may be subject to an employer shared responsibility payment.

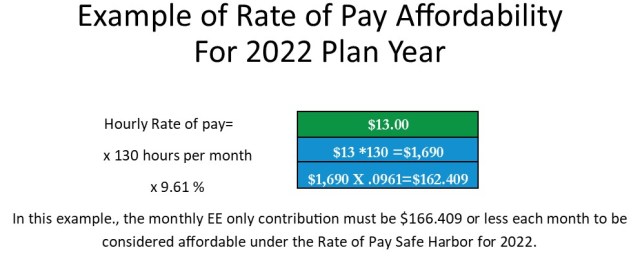

Currently, for 2022, coverage is considered affordable if the employee’s required contribution for employee only coverage on the employer’s lowest-cost plan that offers minimum essential coverage and minimum value, as defined by the ACA does not exceed 9.61% of the employee’s household income. This is a decrease from the 2021 ACA affordability of 9.83%.

If certain conditions are satisfied, an ALE may use one or more of the three affordability safe harbors to determine if it’s offering affordable coverage under the ACA: W-2, Rate of Pay, and Federal Poverty Level (FPL).

An ALE may choose to use one safe harbor for all of its employees or to use different safe harbors for employees in different categories, provided that the categories used are reasonable, and the employer uses one safe harbor on a uniform and consistent basis for all employees in a particular category.

Federal Poverty Level*:

The federal poverty level safe harbor requires just one calculation. Under this safe harbor, coverage is affordable if the employee’s monthly cost for self-only coverage under the plan does not exceed the federal poverty level for a single individual. The employer can ignore the employee’s actual hours and wages, which is very helpful when calculating premiums for a workforce with fluctuating schedules and compensation. But, the federal poverty level safe harbor often results in high-cost sharing by the employer and relatively low premiums for employees.

In 2022, the FPL affordability safe harbor employee contribution amount for calendar year plans an employer can use is $12,880 x 9.61% = $1,237.76/12 =$103.14/mo.

However, the FPL for 2022 non-calendar year plans may be different.

HHS posts the FPL compensation amount annually by February, so the FPL amount used to calculate the safe harbor in December 2021 for a calendar (1/1/2022) plan year, $12,880 was the only FPL compensation level amount available. Whereas, in January 2022, the FPL compensation level changed to $13,590. 9.61% x $13,590 =$1,305.99/12 =$108.83/month.

The IRS recognizes ALE’s need to know well in advance of open enrollment how to set rates, therefore per the final regulations employers are:

“permitted to use the guidelines in effect six months prior to the beginning of the plan year, so as to provide employers with adequate time to establish premium amounts in advance of the plan’s open enrollment period.”

If that six month look-back period reaches into a prior calendar year and two different FPL compensation amounts (and corresponding FPL affordability safe harbor contribution amounts) are available (one from the prior year and the other from the current year), the employer can choose between the two calculations in applying the FPL affordability safe harbor.

Example: A plan that starts June 1, 2022 may “look-back” to the FPL safe harbor in effect 6 months prior which is $103.14/mo, or use the FPL safe harbor in effect using the FPL amount released in 2022, $108.33. Whereas a plan starting September 1, 2022, looking back six months would bring up only one possible FPL safe harbor employee contribution amount the employer may use, $108.33.

Note: When applying the look-back approach, the affordability percentage that applies for the year in which the plan year starts must be used. e.g. Any plan starting in 2022, 9.61% is the percentage that applies even when using the FPL amount ($12,880) for 2021 to do the calculation.

So although you will see articles sharing the FPL in 2022 is $103.14/mo ($12,880x 9.61% = $1,237.76/12), keep in mind this is for calendar year plans and a second FPL amount is available for non-calendar year plans.

If you have questions about the above or need help with another employee benefits administration question, please contact us! We would love to hear from you!

*If in Alaska or Hawaii, the amount used in the above calculations changes from $13,590 to $16,990 & $15,630 respectively.

The Compliance Rundown is not a law firm and cannot dispense legal advice. Anything in this post or on this website is not and should not be construed as legal advice. If you need legal advice, please contact your legal counsel.

Additional resources: