The ACA requires employers with 50 or more employees (i.e., Applicable Large Employers (ALE’s)) to provide affordable coverage to employees working 30 or more hours per week or may be liable for a penalty. Determining affordability is based on looking only at the employee share of the lowest-cost monthly premium for self-only minimum value coverage. It does not include any additional cost for family coverage and if an employer offers more than one health coverage option, affordability applies to the lowest-cost minimum value option. The final “employer shared responsibility regulations include three optional safe harbors that an employer may use.

FEDERAL POVERTY LEVEL (FPL):

The federal poverty level safe harbor requires just one calculation. Under this safe harbor, coverage is affordable if the employee’s monthly cost for self-only coverage under the plan does not exceed the federal poverty level for a single individual. The employer can ignore the employee’s actual hours and wages, which is very helpful when calculating premiums for a workforce with fluctuating schedules and compensation. But, the federal poverty level safe harbor often results in high-cost sharing by the employer and relatively low premiums for employees. In 2021, the FPL for calendar year plans $12,760 x 9.83% = $1,254.31/12 =$104.52/mo is the maximum monthly employee-only premium cost to be affordable for employee-only coverage. However, the FPL for 2021 non-calendar year plans may be different. HHS posts the FPL compensation amount annually by February, so the FPL used to calculate the Safe Harbor in December 2020 for a 1/1/2021 plan year, $12,760 was the only FPL compensation level amount available. Whereas, in February 2021, the FPL compensation level is $12,880 9.83%($12,880)=$1,266.10/12 =$105.50/month. Therefore, the FPL for 2022 calendar year plans is $103.14/month ($12,880 x .0961=$1,237.77/12=$103.14) Federal regulations allow employers to select the applicable FPL compensation amount by looking back 6 months before the first day of their plan year. If that look-back period reaches into a prior calendar year and two different FPL compensation amounts (and corresponding FPL affordability safe harbor contribution amounts) are available (one from the prior year and the other from the current year), the employer can choose between the two calculations in applying the FPL affordability safe harbor.

W-2 SAFE HARBOR:

Under the W-2 safe harbor, an employer looks at each employee’s W-2 for the calendar year (as reported in Box 1). To be affordable, the employee’s required premiums for the employer’s lowest-cost self-only coverage cannot exceed 9.83% for 2021 (9.61% for 2022) of that employee’s W-2 wages. This requires a retrospective analysis of each employee’s W-2 wages. In other words, you don’t know whether you passed the test until it’s too late. Alternatively, an employer could attempt to use the W-2 safe harbor at the beginning of the year by setting premium rates which would ensure that employee contributions would fall below the required threshold. However, it’s very risky to set employee contribution rates based on W-2 wages that cannot be determined until after the end of the year, especially for employees with fluctuating schedules and income. Note: W-2 Box 1 income does not include 401k and cafeteria plan deductions, therefore it’s not equivalent to using the employee’s salary or gross pay.

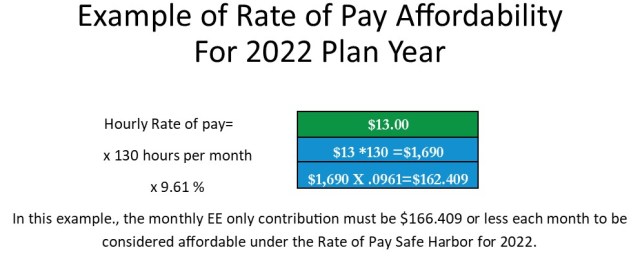

RATE OF PAY SAFE HARBOR:

Rate of pay safe harbor avoids the retrospective analysis of each hourly employee’s W-2 wages because it allows you to assume a rate of 130 hours per calendar month times the employee’s hourly rate of pay. To be affordable, the employee’s required premiums for the employer’s lowest-cost self-only coverage cannot exceed 9.83% for 2021 (9.61% for 2022) of that rate (i.e., 130 hours times the employee’s hourly rate of pay). However, if an employee’s hourly rate of pay is reduced during the year, there are significant limitations on the use of this safe harbor and the calculation of employee premiums. Further, the rate of pay safe harbor is not available for any month that a non-hourly employee’s compensation is reduced, including due to a reduction in work hours. Also, as a practical matter, rate of pay safe harbor cannot be used for tipped employees, commissions or similar compensation arrangements where income fluctuates on a monthly basis.

If you need help in determining whether your plan is affordable or which safe harbor may be best, send an email to: inquiry@compliancerundown.com with the subject line “Affordability Calculator”.

If you have questions about the above or need help with another employee benefits administration question, please contact us! We would love to hear from you!

The Compliance Rundown is not a law firm and cannot dispense legal advice. Anything in this post or on this website is not and should not be construed as legal advice. If you need legal advice, please contact your legal counsel.